ARES Urbanexus Update #161

The American Real Estate Society (ARES) distributes this monthly selection of real estate and community development news and information. H. Pike Oliver curates it.

Residential

Affordability declines in the USA

In 2023, existing residential property sales fell to their lowest level in nearly 30 years, while the median price surged to historic highs, according to a recent report by the National Association of Realtors. Although personal income has risen since the 2000s, it has failed to keep pace with the soaring housing rates, resulting in a widening gap between income growth and home prices. From 2000 to 2023, median income in the U.S. increased by 63.82%, from $41,990 to $68,786 per year, while the median home price surged by 241.49%, from $119,600 to $408,428, as per the latest data from the U.S. Census Bureau.

New homes are getting smaller in the USA

After years of prioritizing large homes, the nation’s biggest and most powerful home builders are finally building smaller ones, driving a shift toward more affordable housing. Census data shows that the boom in smaller construction has cut median new-home sizes by 4 percent in the past year to 2,179 square feet, the lowest reading since 2010. That’s helped reduce overall costs and contributed to a 6 percent dip in new-home prices in the same period. Learn more here.

Perspective on the Low-Income Housing Tax Credit Program in the USA

Building is expensive, and financing is tight in the current multifamily market. However, as it has for the last 30 years, the Low-Income Housing Tax Credit (LIHTC) program provides solutions that increase the ease of creating and sustaining affordable housing, even when the overall multifamily market faces challenges. The program promotes the construction and acquisition of housing and enforces conditions that help maintain the stability and preservation of affordable properties.

Many assume that low-cost housing faces extreme financial risk, but that isn’t true. With LIHTC credits, developers attract corporate investors whose financial investment is returned through tax benefits with no required cash return from the developer or the project. The overall arrangement provides a strong economic advantage to the projects, facilitating the creation of more affordable housing.

These properties also benefit from market conditions and the shortage of affordable rental housing for people in the 60-percent-or-lower area median income (AMI) bracket that the LIHTC program serves. Given the dramatic shortage of affordable housing, an economic downturn does not translate into financial weakness in LIHTC deals. Learn more here.

Office

Return to the office in the USA

A Placer.ai analysis of office building foot traffic over the past several years suggests that the office recovery story is still very much being written. After plummeting during COVID, nationwide office visits began a slow but steady upward climb in 2021, reaching about 70.0% of January 2019 levels in August 2023.

Since then, the recovery appears to have stalled – with some observers even proclaiming the death of return to the office. But looking back at the office visit trajectory since 2019 shows that the process has been anything but linear, with plenty of jumps, dips, and plateaus along the way. And though office foot traffic tapered somewhat between November 2023 and January 2024, this may reflect holiday work patterns and January’s unusually cold and stormy weather rather than any true reversal of RTO gains. Indeed, if 2024 is anything like last year, office visits may experience an additional boost as the year progresses. Learn more here.

Cities face revenue losses as office values fall

In San Francisco, a 20-story office tower that sold for $146 million a decade ago was listed in December 2023 for just $80 million. In Chicago, a 200,000-square-foot-office building in the city’s Clybourn Corridor that sold in 2004 for nearly $90 million was purchased last month for $20 million, a 78 percent markdown. And in Washington, DC, a 12-story building that mixes office and retail space three blocks from the White House that sold for $100 million in 2018 recently went for just $36 million.

Cities are starting to bear the brunt. Municipal budgets that rely on taxes associated with valuable commercial property are now facing shortfalls and contemplating cutbacks as lower property assessments reduce tax bills. A fiscal report published by the National League of Cities last year found that optimism among municipal finance officials has started to wane amid concerns of weaker sales and lower property taxes coinciding with the expiration of federal funds. Learn more here.

It costs too much to turn most offices into homes

A recent posting by Goldman Sachs points out that converting underutilized office space to residential units is harder than it sounds — in large part because it’s expensive. The costs of acquiring and converting commercial buildings are high.

Prices also have not fallen to reflect vacancy rates. Not many properties are changing hands, which is a function of the limited availability of financing as regional banks pull back. Banks, rather than liquidating defaulted loans, have been modifying them to give time to landlords to figure out their plans.

The cost of regulation is also high. Many cities don’t allow commercial buildings to be immediately used for residential purposes. For developers to make that change could be a multi-year drag, which factors into their costs. The Goldman Sachs team’s research indicates that only 0.8% of US office inventory is currently priced at a level that makes conversion to multifamily housing financially feasible. Learn more here.

Retail

Pandemic recovery for restaurants

Derek Thompson of The Atlantic reports that restaurant recovery is not a simple story of universally positive outcomes. In 2020, the restaurant business as we knew it looked like a goner. Even its own lobbying group said so. As the pandemic crushed bars and sit-downs, the National Restaurant Association made a dire prediction: The business would likely never return to its pre-pandemic state.

Given this gauntlet from hell, it is surprising that in 2024, the restaurant recovery overall is complete by almost any measure. Before the pandemic, about 12.3 million people worked in restaurants. Today, about 12.3 million people work in restaurants. Before the pandemic, Americans spent $1.28 on food away from home (mostly at restaurants and bars) for every dollar they spent on food at home (in grocery stores and supermarkets, for example). In 2022, the USDA reported that the away-home ratio for food spending had sprung back to exactly $1.28. The NRA now forecasts that food and beverage sales will hit $1.1 trillion this year, a new record. Arguably, business is booming like never before. Learn more here.

Car washes

Fueled by private equity and a subscription-based business model, the auto wash industry is flooding the US with new outlets. With 60,000 locations across the US, the sector has been expanding at roughly 5% annually, with some forecasts predicting the market to double by 2030. More car washes were built in the last decade than all the preceding years combined. Learn more here.

Regional and metropolitan trends

Where immigrants go in the USA

Much of the angst surrounding the impact of newly arrived migrants on the US has focused on the biggest cities in New York, Illinois, and Colorado, and immigration court records suggest that those states are indeed among the most affected by the surge. The data also signal that Texas and Florida, which have long complained about the costs of absorbing newcomers, are still among the top destinations for migrants. Learn more here.

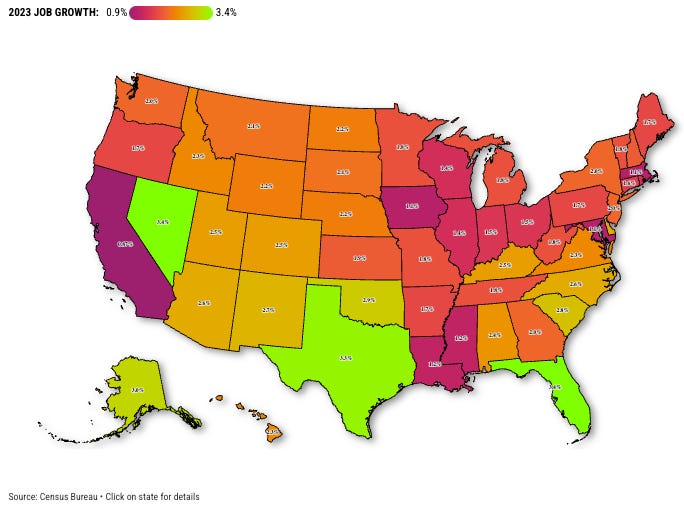

Job growth in states of the USA in 2023

Looking at employment statistics for 50 states and the District of Columbia from the Bureau of Labor Statistics, California added workers at the lowest rate—0.87%. While any job growth is good, that hiring pace looked meager in an otherwise strong US labor market. California’s hiring pace was less than half the 2% rate nationally. Second-slowest was D.C. at 0.91%. The fastest job growth happened in Nevada and Florida, where the increase was 3.4%, and Texas rose 3.3%. Learn more here.

The new job hot-spots

Prior to COVID-19, the West led other regions in job growth, and salaries in major cities commanded a hefty premium over those in smaller counterparts. Cities across the Sunbelt are now adding jobs at a chart-topping rate, while the traditional superstar cities such as San Francisco have had many companies pick up and move, with workers and their employers seeking better living and affordability elsewhere. At the same time, the pay bump that once accompanied a big-city posting has, in many cases, come down to earth, while salaries in other regions have risen. Learn more here.

Metropolitan area growth in the USA

According to a Brookings Institution analysis, growth during the 2012-2022 decade was strongest and most widespread in metro areas with populations over 1 million. Of these 54 “very large” regions, 45 (83%) posted gains across three growth indicators and outpaced the nation on these indicators overall. Very large metro areas also posted uniquely strong gains across measures of economic prosperity, keeping pace with the U.S. average on wage growth and outperforming the nation on productivity (output per job) and standard of living (output per person) gains.

In total, 52 (96%) very large metro areas improved across all these three prosperity metrics—a significantly greater share than midsized metro areas (80%) and large metro areas (89%). Southern and Western metropolitan areas powered U.S. growth during this period, as seen by large gains in real GDP, jobs, and employment at young firms. However, there was significant regional variation in the degree to which growth translated to prosperity. Western metro areas led those in other U.S. regions on average measures of both growth and prosperity, whereas Southern metro areas experienced much smaller increases in average wages, productivity, and standard of living. These divergent outcomes in prosperity suggest a more “population-fueled” growth pattern in the South relative to the West, with population gains fueling economic growth more than improvements in productivity.

Learn more here.

Happiest cities in the USA

Location plays a hand in how bright or gloomy our days are. For years, researchers have studied the science of happiness and found that its key ingredients include a positive mental state, a healthy body, strong social connections, job satisfaction, and financial well-being. However, money can only make you so happy – people who make $75,000 a year won’t get any higher satisfaction from more money.

But not everywhere in the U.S. experiences a uniform level of happiness. WalletHub drew upon the various findings of positive-psychology research in order to determine which among more than 180 of the largest U.S. cities is home to the happiest people in America. They examined each city based on 29 key indicators of happiness, ranging from the depression rate to the income-growth rate to the average leisure time spent per day. Learn more here.

The ten happiest cities

Workers living farther from their employers

A Stanford-Gusto study found that the steadily increasing distance between employees and employers in the U.S. is driven by workers hired after March 2020. In May 2020, after most pandemic lockdowns were put in place, new hires lived an average of 26 miles from their employer. By the end of 2023, that distance had expanded to 35 miles on average. The data includes people who live hundreds of miles away from their employers and likely never make the commute.

The rise in mean distance mainly reflects persons hired since March 2020

Urban design

The urbanist building height myth that won’t die

A video from Oh the Urbanity! YouTube channel dissects the commonly held notion that the ideal building height is a maximum of five stories. It’s Inspired largely by Danish designer and architect Jan Gehl’s landmark text Cities for People, in which he argues that taller buildings are out of scale with the human experience.

But this universal “optimal” or “ideal” building height isn’t based on any objective measure of what urban planners should aim for. Watch the video to view and hear the full critique.

Climate change and sustainability

A green tipping point

According to JLL, real estate is heading toward a “green tipping point.” They say, “The state of play is clear: corporate occupiers must show proof of progress in their commitment to operating more sustainably, and buildings need to catch up.”

On the regulatory side, mandates driving decarbonization are building across all levels of government. The world’s largest economies, including the U.S., California, Canada, UK, EU, Australia, and, most recently, China, have implemented or proposed mandatory ESG disclosure rules, with first reports due by 2026 or earlier. These rules aim to improve transparency and accountability for the biggest companies around the globe while promoting the transition to a net zero economy.

Policy directly requiring emissions reductions from buildings is ramping up. For example, over 30 U.S. cities have committed to passing a Building Performance Standard (BPS) by 2024, like New York’s LL97, requiring building energy use or emissions reductions. In Europe, the EU agreed in December 2023 to reduce building emissions and energy use by developing minimum energy performance standards. Some 16% of the worst-performing buildings will need renovating by 2030 and 26% by 2033.

Learn more here.