ARES Urbanexus Update #169

The American Real Estate Society (ARES) distributes this monthly newsletter, which features news and information about real estate and metropolitan development curated by H. Pike Oliver.

Office

Tech, especially AI, is driving U.S. office leasing

The tech industry boosted its share of U.S. office leasing to 18% in the first three quarters of this year, partly fueled by companies involved in artificial intelligence (AI). CBRE’s Tech-30 report analyzes the tech sector's influence on office demand and rental rates across 30 major tech markets in the U.S. and Canada, as well as select submarkets.

This 18% share marks a 3.8 percentage point rise from the 14.2% recorded for all of 2023, placing tech ahead of Finance & Insurance (16.5%) and Professional & Business Services (15.7%). After trailing both industries in 2022 and early 2023, tech regained the lead in last year's third quarter and has now held the top position for five consecutive quarters.

This year marks a comeback for the tech industry, following layoffs in 2023 and a slowdown in U.S. venture capital funding from 2021 to 2023. Tech job growth rose by 1% in the first seven months of the year, compared to 0.3% in 2023. Venture capital funding, particularly for AI companies, increased 13.3% year-over-year in the first half of 2024, and large-cap tech stocks lifted the Nasdaq stock index.

Learn more here.

Residential

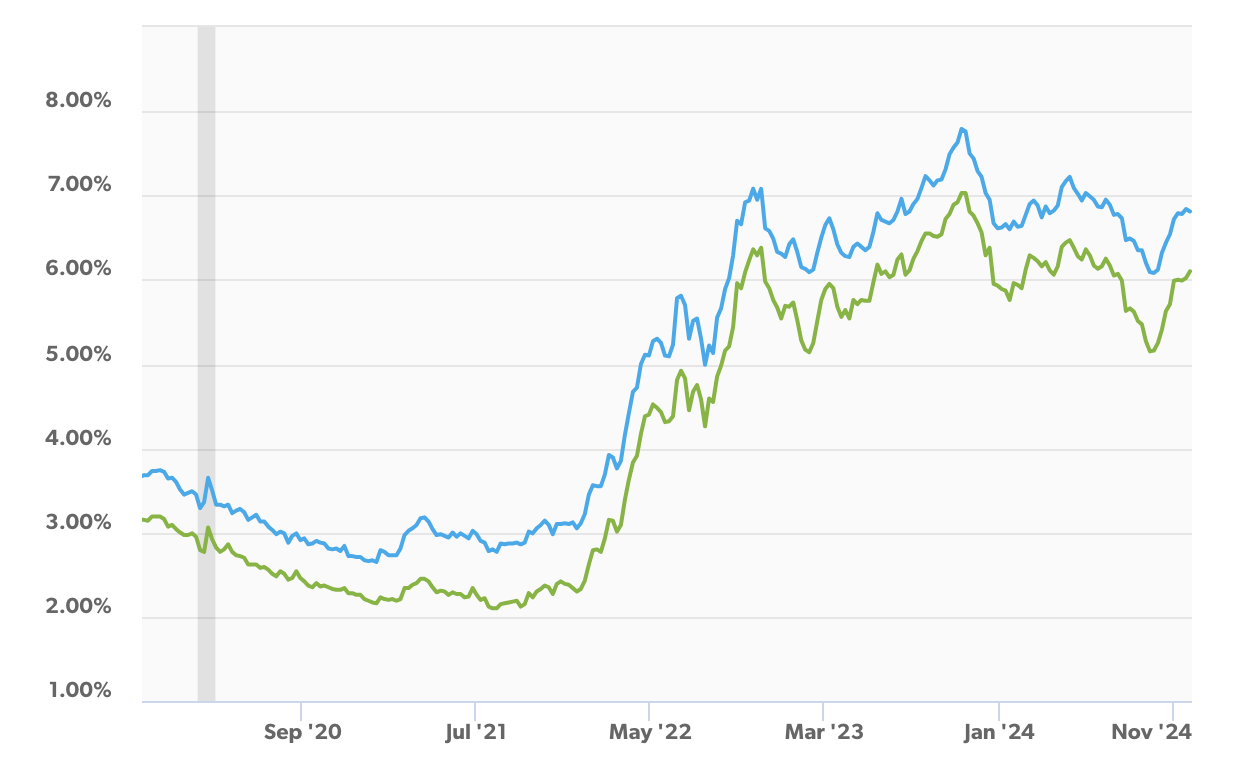

U.S. mortgage rates remain high

Based on Freddie Mac's latest Primary Mortgage Market Survey (PMMS), the 30-year fixed-rate mortgage (FRM) averaged 6.78 percent as of November 14, 2024

As of Thanksgiving 2024, the 30-year FRM averaged 6.81 percent, down from 7.44 percent in November 2023.

The 15-year FRM averaged 6.01 percent; in November 2023, it averaged 6.76 percent.

Learn more here.

House payments vs. household income in the USA

In another sign of America’s ongoing housing affordability crisis, the National Association of Home Builders /Wells Fargo Cost of Housing Index (CHI) found that in the third quarter of 2024, a family earning the nation’s median income of $97,800 needed 38% of their income to cover the mortgage payment on a median-priced new home. Low-income families, earning only 50% of the median income, would have to spend 75% to pay for the same new home.

The figures track identically for the purchase of existing homes. A typical family would have to pay 38% of their income for a median-priced existing home, while a low-income family would need to pay 75% to make the same mortgage payment.

Learn more here.

Retail

Bifurcation away from the “middle”

Consumers increasingly gravitate toward luxury or value offerings and away from the ‘middle.’ Add extended economic uncertainty, rapid expansions, and product diversification from top value-oriented retailers, and you have an explosion of visits to the value lane.

But there is a ceiling to that growth, especially in the discount and dollar store space. Throughout 2023 and the first part of 2024, visits to discount and dollar stores increased steadily. However, no category can sustain uninterrupted visit growth forever. Since April 2024, year–over–year (YoY) foot traffic to the segment has begun to slow, with September 2024 showing just a modest 0.8% YoY visit increase.

Learn more here.

Cost-conscious consumers and value grocers

The rising cost of living has pushed the discount retail segment into overdrive, and value grocery chains are also benefiting. The category has flourished in recent years, with many bargain-oriented grocery chains adding new stores quickly to meet burgeoning consumer demand.

Like visitors to specialty grocery chains, value shoppers demonstrate segment-specific behaviors that reflect their preferences and habits. And perhaps most strikingly, foot traffic data reveals that these shoppers tend to stay longer in-store than visitors to traditional and specialty grocery chains.

In Q3 2024, 26.5% of visits to value grocery chains lasted longer than 30 minutes, compared to 23.4% for traditional grocery chains and 23.7% for specialty and fresh-format chains. This suggests that these stores attract shoppers who take their time and carefully consider price points, looking for the best value for their dollar—a need that the chains they frequent seem to be meeting.

Learn more here.

Real estate finance

Growth in lending

Research by CBRE shows that the commercial real estate lending market continued its upward trajectory in the third quarter of 2024. There was a notable increase in acquisition financing and strong issuance across asset classes, including large office transactions.

The CBRE Lending Momentum Index, which monitors the rate of CBRE-originated commercial loan closings in the U.S., rose by 13% from Q2 2024 and by 15% year-over-year, indicating enhanced lending activity. The index closed Q3 2024 at 214, approaching the pre-pandemic five-year average of 229.

In Q3 2024, the average spread on closed commercial mortgage loans was 183 basis points (bps), down 35 bps from the previous year and stable from Q2 2024. Multifamily loan spreads narrowed slightly to 168 bps for the quarter.

Learn more here.

Climate change

Changing weather degrades buildings

Longer, more severe heat waves degrade roofs and strain air conditioning and HVAC systems. Wild temperature swings bring thermal cycling that expands and contracts concrete and masonry walls, hastening cracks and water intrusion. Asphalt shingles, the most common covering on residential homes in the US, warp under an unrelenting sun, while pavement buckles, steel rails, kink, and siding suffer “solar distortion.” Foundations can shift in drought or high temperatures, leading to cracked walls, burst pipes, and serious structural problems.

Trepp, a real estate analysis firm, found that repair and maintenance costs were up 30% last year in many major US markets, including Dallas, San Francisco, San Diego, and Houston. One study by Atlas Real Estate found the average cost of repairs in rental property — driven by material costs, inflation, and labor costs — rose from $290 per incident in 2018 to $501 in 2024. And, unlike floods or storm damage, insurance often doesn’t cover these problems.

Learn more here.

Resilience and sustainability

Ten principles for building resilience

A 2018 Urban Land Institute publication considers the economic, environmental, and social factors that contribute to resilience and how the concept of resilience translates to the private sector, municipal decision-makers, and communities. Ten Principles for Building Resilience equips real estate developers and asset managers, city officials, city leaders, and the public to address vulnerabilities and enhance resilience as relevant to their communities, real estate projects, and broader civic involvement.

The Ten Principles include:

Understand vulnerabilities

Strengthen job and housing opportunities

Promote equity

Leverage community assets

Redefine how and where to build

Build the business case

Accurately price the cost of inaction

Design with natural systems

Maximize co-benefits

Harness innovation and technology

You may download the report here.

Adaptive reuse in Paris

There is a remarkable trend of old buildings being converted to new housing in Paris. Some of the city’s major social housing developers have made adaptive reuse a central part of their strategy for adding new housing. See Brian Googin’s post to his Substack Housing in Practice to see several recent examples, including a conversion of military barracks to social housing.

Metropolitan and regional trends

Hope for U.S. factory towns

For much of the last half-century, economic life in manufacturing regions of the U.S. has been dominated by factory closings, joblessness, and downgraded expectations. Textile mills and furniture plants have been undercut by low-priced imports from Mexico and China, and tobacco processing jobs have disappeared. Yet over the last several years, an infusion of investment in cutting-edge industries like biotechnology, computer chips, and electric vehicles has lifted the fortunes of long-struggling communities.

North Carolina presents a conspicuous example of this trend, yet a similar story is playing out elsewhere. From industrial swaths of the Midwest to factory towns in the South, areas that suffered the most wrenching downsides of trade are now capturing significant shares of investment into forward-leaning industries, according to research from the Brookings Institution, a public policy research organization in Washington.

Learn more here.

Around the world

Foreclosures in China soar

Banks in China are foreclosing on apartments after homeowners could not pay their mortgages, as the country’s housing crash threatens the financial system. According to official data, the roster of homes seized and listed for auction leaped 43 percent last year. Numerous Chinese banks have disclosed increases in mortgage defaults during the first half of this year.

Foreclosures are a sensitive subject in China, where the government keeps a tight grip on society. Regulators adopted new rules that make it hard for banks to evict some defaulting homeowners. Bidders who buy apartments in foreclosure auctions must often purchase the apartments sight unseen and then work with neighborhood officials to persuade the occupants to leave.

Real estate prices have fallen almost 30 percent from their peak in 2021. In China, banks and the government wonder how much worse the problem could get.

Learn more here.