ARES Urbanexus Update #168

The American Real Estate Society (ARES) distributes this monthly selection of real estate and metropolitan development news and information curated by H. Pike Oliver.

Industrial

7,000 robots in a big Amazon warehouse

In Southern California’s Inland Empire, a region accustomed to Amazon’s smiling arrow logo on warehouse buildings, the scale of the online retailer’s latest warehouse stands out. At six stories and roughly 4.5 million square feet, the Robotics Sortable Fulfillment Center in Ontario is Amazon’s largest U.S. facility.

Besides its size, the Baker Avenue complex in Ontario, CA, is special for another reason — more than 7,000 robots help the warehouse’s 2,000-plus human workforce process as many as 1 million daily shipments. The warehouse, which can hold up to 50 million items, receives, unpacks, packs, and sends a wide range of consumer goods to points locally, nationwide, and worldwide.

Learn more here.

A changing industrial market in the USA

The nation's industrial market slowed in the third quarter of 2024, building on a two-year cooling-off period after its pandemic heyday, but the market could soon hit bottom. Preliminary data from Savills found the U.S. industrial vacancy rate hit 7.4% in Q3 2024, a 350-basis-point increase from Q3 2022. It's also the highest vacancy rate within the U.S. industrial market in a decade.

In response to the slowing market, new construction has declined, with starts in Q3 hitting their lowest level since 2016. According to Cushman & Wakefield PLC (NYSE: CWK), as of the third quarter of 2024, 309.3 million square feet of industrial space nationally was under construction, the lowest level since the end of 2018.

Learn more here.

Nearshoring

According to Henry Steinberg, Global Head of EQT Exeter, the biggest lesson from the COVID-19 pandemic for investors in industrial real estate is that proximity matters. Businesses want to be closer to their customers, whether they are a medical company distributing vaccines or a manufacturer producing chips. That means they need more warehouse space, industrial land, and power.

Nearshoring is reshaping the warehouse real estate market. According to Steinberg, it is a structural shift in how businesses manage their supply chains. As more companies look to diversify and de-risk their operations, nearshoring may continue to drive demand for industrial real estate in the U.S. and Mexico.

Learn more here.

Office

Converting offices to dorm-syle co-living

The United States has a shortage of 4 million to 7 million homes and, at the same time, an all-time-high office vacancy rate of 20%, meaning that more than a billion square feet of office space is unused. However, despite the urgent need for housing and policymakers’ desire to convert underused office space to apartments to help revitalize downtowns that lost residents and businesses during the pandemic, construction costs remain too high to make most such conversions profitable.

New research from The Pew Charitable Trusts and Gensler, the global architecture, design, and planning firm, has identified a more economically viable approach to office-to-residential conversions. It employs a design that reduces construction costs and enables affordable lower rents for people earning less than an area’s median income.

The design calls for converting buildings to co-living dorm-style apartments rather than conventional apartments. Each floor features private, locked “microunits” along the perimeter, with shared kitchens, bathrooms, laundry, and living rooms in the center.

You may learn more here.

Climate and environment

Decarbonizing building operations

The real estate industry faces growing pressure to reduce the emissions caused by building operations. The good news is that the technology already exists to solve the problem, and a new way to formulate decarbonization plans can make it easier and more cost-effective to take action, as McKinsey partner Brodie Boland discusses with McKinsey Global Publishing’s Katy McLaughlin.

The real estate industry accounts for approximately 40 percent of global combustion-related emissions, of which over 25 percentage points come from building operations. That means most of the emissions come from running buildings rather than building them.

So here’s the good news: it’s often possible to achieve full operational net-zero emissions in a financially neutral or positive way. The ways to do it exist at scale today and do not require newfangled technologies. Viable approaches include heat pumps, the electrification of heating, cooling, and cooking elements, improved building envelopes and better insulation, and installation of on-site renewable sources such as solar panels. In some cases, it involves installing widely available devices that can do things like turn the lights off when people leave a room.

Learn more here.

A builder’s guide to carbon-neutral construction

There are three key strategies to lower—to zero and even negative—the amount of embodied carbon in our buildings: reusing infrastructure, designing to minimize carbon emissions, and using lower-carbon materials. And since reducing upfront carbon is an additive process, you can use these approaches individually or in any combination to reduce a building’s overall carbon footprint.

See the graphic below and learn more from Craig Savage’s Journal of Light Construction article here.1

Moving into climate-risk areas in the USA

These U.S. counties regularly experience hurricanes, major wildfires and floods, and punishing heat. They’ve been some of the most popular places to move for two decades as Americans have flocked to the South and West. The country’s vast population shift has left more people exposed to the risk of natural hazards and dangerous heat at a time when climate change is amplifying many weather extremes.

A New York Times analysis highlights the dynamic in new detail:

• Florida, regularly raked by Atlantic hurricanes, gained millions of new residents between 2000 and 2023.

• Phoenix has been one of the country’s fastest-growing large cities for years. It’s also one of the hottest, registering 100 straight days with temperatures above 100 degrees Fahrenheit this year.

• The fire-prone foothills of California’s Sierra Nevada have seen an influx of people even as wildfires in the region become more frequent and severe.

• East Texas metro areas, like Houston, Austin and Dallas-Fort Worth, have ballooned in recent decades despite each being at high risk for multiple hazards, a fact brought into stark relief this year when Hurricane Beryl knocked out power in Houston during a heat wave.

Learn more here.

Climate-fueled disasters across the USA

Across the US, natural catastrophes are becoming more expensive and more common. Global warming supercharges the atmosphere with more water and energy, fueling increasingly violent weather. Destructive storms, droughts, floods, and wildfires are colliding with communities where millions of people live, with more costly homes and possessions—and so much more to lose. Learn more here.

Real estate decarbonization in the USA

A coalition of leading sustainable building organizations has released a detailed agenda for the next presidential administration. The U.S. Green Building Council (USGBC), New Buildings Institute (NBI), Institute for Market Transformation (IMT), and Carbon Leadership Forum (CLF) collaborated to develop the recommendations. The agenda aims to help commercial buildings recover from the current downturn and better prepare for the future.

Specifically, the agenda calls for expanding the Sec. 48E Clean Electricity Investment Tax Credit (ITC) in the U.S. to cover energy efficiency investments. The ITC currently covers only electricity-generating technologies, such as on-site solar, even as energy efficiency is widely viewed as a foundational solution to energy and climate challenges.

The proposed expansion would drive significant economic activity in retrofitting buildings to be more energy efficient and provide parity under the tax code for energy efficiency as the ITC transitions to a technology-neutral structure in 2025. It would also reduce demand on the grid and accelerate our ability to meet clean energy targets.

Learn more here.

Planning

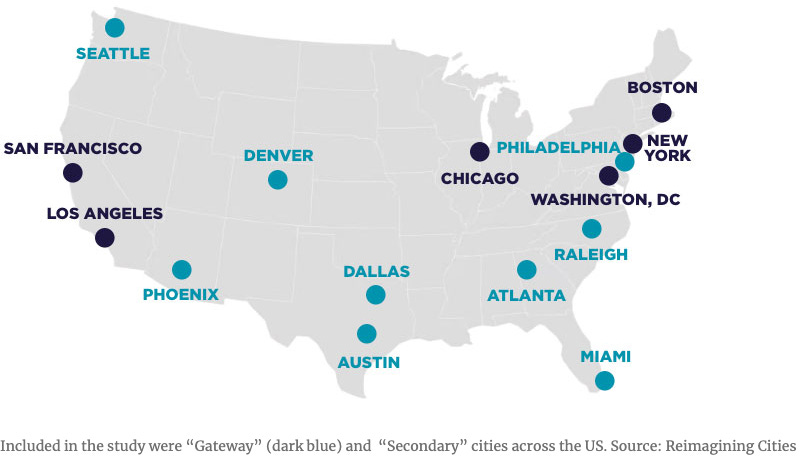

Reversing the “urban doom loop”

A recently released report, Reiminaging Cities: Disrupting the Urban Doom Loop, from Cushman & Wakefield with Christopher Leinberger and Places Platform, analyzes 208 regionally significant urban centers in 15 major metro areas across the US. These centers include four types of WalkUPs: downtowns, downtown adjacent, urban commercial, and urban universities.

These walkable centers are efficient economic engines: They comprise only 3 percent of the land but generate 57 percent of the GDP in these cities. “One could argue that these WalkUPs are the reason the city exists,” says Leinberger. Better functioning WalkUPs would improve the nation’s economy, the report argues.

The “doom loop” results from WalkUPs putting “too many eggs in the office basket.” The report concludes that using portfolio theory to rebalance real estate toward less office space (work), more play (culture, entertainment, retail), and more residential (especially for-sale housing) would shift these urban centers back to the positive economic track they were on before COVID.

You may download the report here.

The high cost of excess parking

Look at almost any city’s zoning code in North America, and you’ll find a table of parking ratios, usually dating back 50 to 80 years, mandating a predetermined number of parking spaces for all new buildings —and for every new bedroom, church pew, or bowling lane. If new developments were built with “adequate” off-street parking, the thinking would be that cars and curbsides could be managed. However, one-size-fits-all mandates, determined by city planning offices, were the wrong tool for the job. Guessing at the right numbers, most jurisdictions erred on the side of excess.

Beyond creating an oversupply— parking that doesn’t get used—mandating too much parking carries a raft of unintended consequences. Too much required parking outlaws the kinds of buildings that define cities’ historic, walkable neighborhoods, blunts housing construction, drives up home prices and rents, and increases barriers for entrepreneurs who want to invest in their community. Instead of managing on-street parking, these regulations have locked cities into patterns of sprawling development that make traveling without a car impossible.

Parking is expensive to build. On the low end, a surface parking lot might cost $5,000 to $20,000 per space. A multilevel parking garage can cost $60,000 (or more) per spot. Those costs are passed down, rolled into the price of food, rent, and taxes, whether you park a car there or not. Every parking spot per home can increase rent by 12.5 percent2 (or more than $200 per month3).

Parking costs us in dollars and space. A good rule of thumb is that parking lots must be as large as the building they serve when mandates reach three parking spaces per 1,000 square feet, with 330 square feet[8] for each space. That is a common value. Of the localities studied for a recent report by the Seattle-based Sightline Institute, 61 percent required at least that much parking for offices, and 80 percent required that minimum for stores. Restaurants have it even worse: the typical jurisdiction requires parking lots to be 3.3 times larger than the eatery itself.

Learn more here.

Savage, C. (2022, November 17). A builder’s guide to carbon-neutral building practices. JLC Online. https://www.jlconline.com/how-to/reducing-carbon_o

Todd Litman, “Parking Requirement Impacts on Housing Affordability,” Victoria Transport Policy Institute, January 20, 2009. http://reconnectingamerica.org/assets/Uploads/parking_housing_2009.pdf

Seth Goodman, “How Much Does One Parking Spot Add to Rent?” Reinventing Parking, June 2, 2015. https://www.reinventingparking. org/2015/06/how-much-does-one-parking-spotadd-to.html.